Why Timing Matters in College Financial Aid Planning

Apr 02, 2026

Why Timing Matters in College Planning

The earlier you start, the more options you have

When it comes to college financial aid, timing matters more than most families realize. Income is based on tax returns from two years before college, assets take time to reposition, and financial aid is recalculated every year. The earlier you start planning, the more options you have — and the more options you have, the more control you have over what college actually costs.

When I See “Senior” on My Calendar

I get a notification every time someone books an appointment on my calendar.

As part of the booking process, families fill out a short questionnaire. One of the questions asks what year their student is currently in high school.

I’ll let you in on my thought process when I read “Senior.”

What can we do to improve the financial aid outcome for parents of seniors?

Very little — at least for the first year of college.

Yet nearly half of the appointments that appear on my calendar are from parents of seniors.

And to be clear, I don’t judge the situation at all.

Life happens. You’re busy. Teenagers change direction. Suddenly, a family that thought college might not be necessary is staring at a very large bill.

Income Timing (The Prior-Prior Year)

One of the biggest surprises for families is how income is used in financial aid calculations.

Financial aid is largely based on Adjusted Gross Income (AGI), which is Line 11 on your tax return.

For a student’s first year of college, the system uses something called the prior-prior year, meaning the tax return from two years before college begins.

For example, if your student starts college in 2030, the FAFSA will use your 2028 tax return.

Another way I explain this is that the tax year in question typically spans:

- The second half of your student’s sophomore year

- The first half of their junior year

Financial aid income is based on the tax return from two years before college begins.

As you can see, by the time senior year arrives, the income year used for the first year of college is already locked in.

Asset Timing

Assets work very differently from income.

Income is historical. Assets are a snapshot in time.

Your assets are reported based on their value the day you submit the FAFSA or CSS Profile.

That might sound like good news, but many asset strategies take time to implement properly. They often involve tax planning, documentation, or coordination with financial advisors.

The Annual Reset

Financial aid is recalculated every year your student is in college.

Families sometimes assume they can fix things later if they missed the first opportunity, but the first year often sets the tone for the remaining years.

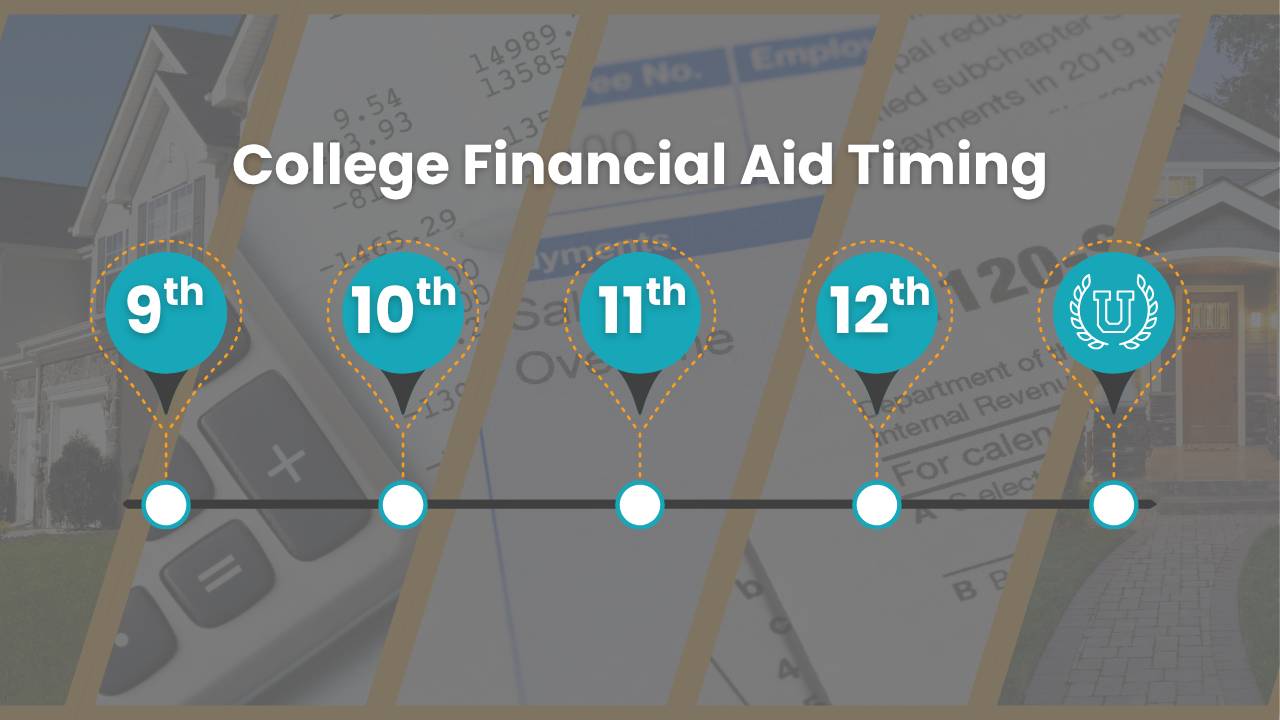

The Planning Timeline

For many families, this general timeline works well:

- 9th Grade: Start learning how financial aid works and review state aid programs.

- Sophomore Year: The income window is approaching. Income strategies should begin.

- Junior Year: The key tax year is closing. Strategies should already be in place.

- Senior Year: Application time. Most financial variables are now largely set.

Think of It Like a Funnel

I often ask families to picture this timeline as a funnel.

At the top of the funnel — during the earlier high school years — the opening is wide. There is flexibility. There are options.

As each year passes, the funnel narrows.

By the time senior year arrives, the opening is very small, and the number of possible adjustments is limited.

So When Should Families Start?

You don’t need to start planning when your children are toddlers.

But for most families, starting in 9th or 10th grade gives you time, flexibility, and options.

And in college planning, options are everything.

Because the families who have the most options are usually the families who end up paying the least.

Grab Our Free College Planning Timeline for Parents

If this article helped you see why timing matters, we created a free download to make the high school years easier to navigate.

It walks parents through what to pay attention to during each year of high school so you can stay ahead of the process without feeling overwhelmed.

Get the Free Download